Oliver is co-founder and CEO of Envestors, an FCA-regulated investment specialist platform. Oliver sits on the board of the UK Crowdfunding Association (UKCFA).

From 2006 to 2014, he also sat on the board of the UK Business Angels Association (UKBAA). Oliver had also found time to sit for an MBA in entrepreneurship at Imperial College, London, when he and his brother were building Woolleys. He is a Member of Court there, also giving the occasional lecture on entrepreneurship.

Early career:

Oliver grew up in Sussex and studied for a degree in finance at Bristol Polytechnic, now the University of West of England, planning to become an accountant. However, travelling in Rajasthan, Oliver was struck by the realisation that being an accountant was not what he wanted to do with his life.

Instead, Oliver decided to set up a food business with his brother. Food was an area they were both passionate about. His brother was the chef, and Oliver dealt with the business side.

Woolleys:

In 1988, they opened a sandwich shop in Central London. This expanded to become the Woolleys Health-foods chain. They added three shops, a health-food store, and catering kitchens with a capacity for 5,000 lunches a day. It was just before the rise of healthy food, but natural quality ingredients made Woolleys a considerable success.

The brothers also opened a small chain of speciality sausage shops across East Sussex. They produced up to a tonne of Hugo Oliver Sausages a week. The successful produce was sold to restaurants, pubs, and various outlets across the South East, including Harrods.

Everything changed when Oliver’s brother had a severe car accident. When Northern Foods made them an offer for both companies a year afterwards in 1997, it seemed timely to sell in every way.

First experiences of Investment:

To fund Woolleys, Oliver had experienced raising equity and bank debt for the first time. After the sale of Woolleys, he tried his hand at early-stage investing. He made three small investments, all three of which went bust.

After these investment experiences had all led to nothing, Oliver decided there had to be a better way of enabling early-stage fund-raising for all parties. He had seen for himself that there were two significant issues.

One issue was deal flow, with investors often restricted to deals they could find via friends or family. The second problem was knowledge, or rather lack of it, about investment deals. Oliver says he was clueless about investing, and the three companies were equally clueless about raising finance.

The result of those experiences was the co-founding of Envestors, launched in April 2004.

Envestors®:

Oliver and two co-founders started small, with 100k between them. They aimed to educate both the investor and the fundraising company. Oliver quickly learned that the three deals he had done had gone through proper corporate finance routes, as they now supply, the problems in all three would have been flagged and either put right, or the deals would never have happened.

They also quickly learned that there were significant challenges in ensuring that everything was appropriately regulated. For Oliver, it was always primary that the Financial Conduct Authority fully licensed them. Doing so provided early challenges to ensure the platform they created met those standards, and it quickly became apparent they would have to create what was needed themselves.

Oliver believes that all deals and activities around them should be regulated, and high standards set and adhered to. Surprisingly, many incubators and accelerators are not doing so. Pitch events also often run outside the rules, arguing that they are only facilitating places to meet, and it is up to all involved to do their own due diligence in every way.

Envestors was sold to Braveheart PLC in 2010. However, in 2014, Braveheart approached Oliver and struck a deal where the ownership reverted. Oliver says he remains surprised to find himself running a tech company, but has brilliant specialist people around him.

Meanwhile, other companies could see the headaches involved in software meeting the legislation requirements. They asked to license Envestors instead. The Envestors’ platform now supports several other investor groups on their platform, including OBN Ventures, Kickstart, Stakeholderz. Oliver told me that while the original stand-alone platform was a challenge. When you need to connect that to a complex of other platforms that have come on board, things get seriously hard. This is an example of why their enormous growth has not been all “beer and skittles,” as Oliver puts it.

Envestors now has a community of 6,000 entrepreneurs looking to scale up and connect with investors. They have their own private investors club and see around 100 proposals a month. Envestors have also raised £2m backing themselves recently to broaden their partnership network of universities, incubators, angels, and larger enterprises and develop their readiness services on the Envestry Platform.

The platform has raised over £100m and helped over 200 businesses.

Envestors’ differential lies in connecting already existing sources of finance and collating them all in one place rather than the scattered approach which exists outside it. They offer companies different packages of advice from essential legalities to handholding throughout a deal being brokered.

Oliver’s aim is that Envestors become the one marketplace for both sides looking to make investment deals. Their expertise is predominantly in the UK markets. As an approved endorsing body for investment visas, they also have clients in China, India, and the UAE.

Envestors have a higher success rate and a lower failure rate with the companies they broker deals for.

| Envestors | The Market | Diff. | |

| Successes (30%+ IRR) | 12% | 9% | +3% |

| Middle-ing (0%-29% IRR) | 67% | 35% | +32% |

| Failures | 21% | 56% | -35% |

Oliver’s Advice:

These are tough times, and that includes raising investment. However, there is investment to be had. Recessions have a reputation for starting great companies and being the land of opportunity. The UK has fantastic tax breaks for investors and a really strong reputation for tech companies.

Investment has become a hugely complex business now, and one that the unguided novice can quickly fail in. There are VCs and Angels, Early Stage Funds, Government Funds, Regional Funds, and International Investors. And these days, Oliver advises that every company should at least consider crowdfunding as an option.

One of the keys is to raise the right money at the right time: start-up and pre-trade funds are for £150-500k, early-stage for 250- 750k, post-revenue for 500k to 2m and then 1m to 5m for growth.

The business angel game is not always sustainable. Most Angels stay in for around 18 months. Currently, the majority are nursing their current deals and need something incredibly special to get them out of their armchairs. That means at the very least a 3, 5 or 10x return.

I asked Oliver what the worst mistakes he sees companies make when they seek investment are.

- As I had expected, the right valuation came high on the list. Oliver says, “Entrepreneurs pay too little attention to their company’s capital structure and the pre-money valuation round.” They then base valuations on their earnings and cash flow models. Investors look at the investment to date and typical market valuations of similar companies in that sector to determine the company’s worth. The valuation will determine how many shares you are letting go of, so it has to be genuinely defensible. Too high a first valuation may sound fantastic, but it is dangerous as it will cause problems for Series A down the line. Mostly over-optimistic valuations simply kill the chance of investment.

- Oliver’s next point is that investors want investor-ready decks, not business plans. He says they regularly receive business plans, which are all about the business and not much about the investment opportunity. Many entrepreneurs seem to mistakenly believe investors to be philanthropists, rather than people seeking a return on their investment. More than ever, the returns need to be especially appealing for investors to take the risk. They are looking for companies with answers to big problems, giving a promise of high growth. Lifestyle businesses are of no interest. The value proposition must be strong, starting with a show-stopping elevator pitch and sound knowledge of your market.

- The whole deal needs to be packaged in a way that appeals to what that particular investor is looking for and as an opportunity that would suit them. Part of that has to include a clear vision of the exit plan and how the investor will be able to take out the massive profits they are going to make. Lack of alignment on exit is a deal-breaker.

- Raising investment takes time, much longer than people expect. Six to nine months is realistic, so early planning is essential. Crowdfunding platforms give companies a three-week window when, actually, fundraising is a continual and ongoing process, which can be an issue. It is also why some companies license Envestors’ FCA-regulated fundraising platform for a full 12-month period, which might initially look excessive.

- The team is crucial. Investors look for a full-time management team of at least two, with proven experience in a management role, and both are going to be entirely focused on the business. An independent Chair and a NED should be on the board. Oliver finds that investors are wary of entrepreneurs with “Founder, CEO, and Chairman” on their business cards. They fear that poor corporate governance will lead to the ignoring of investors’ interests.

- Part of the work Envestors does with their clients is to ensure that there is complete transparency early on. No investor is going to be happy to find at the end of the pitch that the director, not the company, own vital IP; that there are colossal director’s loans in place; that the directors are on employee contracts; there are outstanding disputes. Even with a company pre-trading, the pitch must include a balance sheet to reveal how the company has been set up. It is needed to show what money has gone in and what way, be it loans or to buy equity.

- Legalities are all important. Oliver advises working with both an accountant and a solicitor who regularly work on investment deals from the beginning. The articles and shareholders’ agreements must be part of the pitch, and tag and drag rights in the shareholders’ agreements must be clear. There is tax to be considered. A deal has to be EIS or SEIS fit. If there is the possibility of R and D tax relief offered for manufacturing, design, or software development fields, that could be hugely important.

- Finally, Oliver reminds us – investors don’t fall out of trees. You need to market to investors, just as you would sell to customers. You need to research who you are pitching to, what type of investor, be it, Angel, VC, or crowdfunding. Each type offers different levels of involvement and looks for different things in their investments. Look at the potential investors’ portfolio to learn more about them.

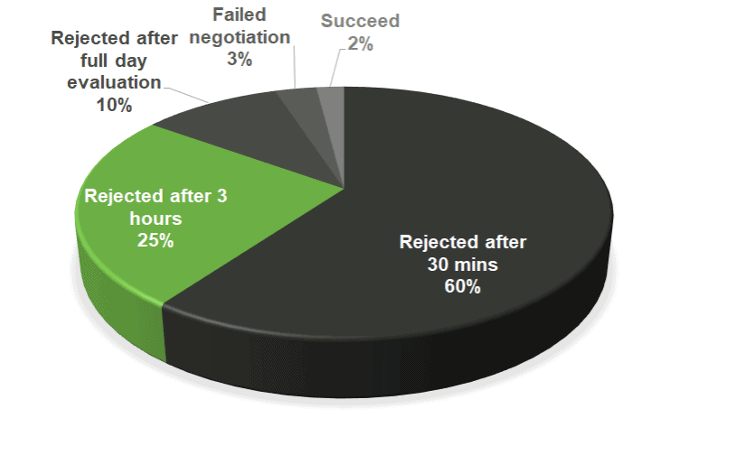

Remember that outside friends and family, raising finance has only a 2% success rate. A large part of success lies in getting the preparation done right and remembering that the investor needs an exceptionally strong reason to invest.

You might also enjoy this about another entrepreneur who has ended up running a tech company when they never expected to.